Time-uniform, nonparametric, nonasymptotic confidence sequences

Steven R. Howard $^{1}$ Aaditya Ramdas $^{2,3}$ Jon McAuliffe $^{1,4}$ Jasjeet Sekhon $^{1,5}$

Departments of Statistics $^{1}$ and Political Science $^{5}$, UC Berkeley

Departments of Statistics and Data Science $^{2}$ and Machine Learning $^{3}$, Carnegie Mellon

The Voleon Group $^{4}$

{stevehoward,jonmcauliffe,sekhon}@berkeley.edu, [email protected]

August 9, 2022

Abstract

A confidence sequence is a sequence of confidence intervals that is uniformly valid over an unbounded time horizon. Our work develops confidence sequences whose widths go to zero, with nonasymptotic coverage guarantees under nonparametric conditions. We draw connections between the Cramér-Chernoff method for exponential concentration, the law of the iterated logarithm (LIL), and the sequential probability ratio test---our confidence sequences are time-uniform extensions of the first; provide tight, nonasymptotic characterizations of the second; and generalize the third to nonparametric settings, including sub-Gaussian and Bernstein conditions, self-normalized processes, and matrix martingales. We illustrate the generality of our proof techniques by deriving an empirical-Bernstein bound growing at a LIL rate, as well as a novel upper LIL for the maximum eigenvalue of a sum of random matrices. Finally, we apply our methods to covariance matrix estimation and to estimation of sample average treatment effect under the Neyman-Rubin potential outcomes model.

Executive Summary: In today's data-driven world, organizations routinely run sequential experiments like A/B tests to optimize online products and services. These tests generate data continuously as users interact, but traditional statistical methods treat the sample as fixed from the start. Peeking at results mid-experiment inflates the risk of false positives—declaring an effect real when it's not—often by a factor of two or more. This problem has grown urgent with the scale of modern experiments, where decisions must be timely and reliable, yet most analyses still ignore the sequential nature of the data.

This paper develops confidence sequences, a tool for building updating confidence intervals that remain valid no matter how long the experiment runs or when it stops. The goal is to create intervals that shrink toward the true value over time, under minimal assumptions about the data's distribution, ensuring at least 95% coverage (or whatever level is chosen) uniformly across all time points.

The authors use a high-level approach rooted in martingale theory—a way to track cumulative deviations in data streams—and connect it to classic ideas like exponential concentration bounds and the law of iterated logarithm. They focus on nonparametric settings, meaning no strong assumptions about data shape, and derive sequences for various cases, including bounded data, heavy-tailed distributions, matrix observations, and causal effects. Key tools include "stitching" linear bounds into curved ones over time epochs, mixture methods for exact boundaries, and self-normalization to estimate variance empirically. They test these on simulated data from independent observations over up to 100,000 points, comparing against fixed-sample and pointwise methods.

The core findings are fourfold. First, the methods yield intervals about twice as wide as standard fixed-sample ones but shrink at a rate of roughly the square root of (log log t over t), matching the theoretical limit from the law of iterated logarithm—far better than non-shrinking bounds. Second, an empirical-Bernstein version adapts to the data's true variance, making intervals 40-50% narrower than conservative bounds based on maximum possible spread, especially for low-variance or skewed data. Third, applications show novel results: for causal inference in randomized trials, intervals track average treatment effects with coverage staying flat at the target level, even under adaptive designs; for covariance matrices from vectors, operator-norm errors are bounded uniformly with a log log t factor added to fixed-sample rates. Fourth, simulations across Bernoulli, heavy-tailed, and three-point distributions confirm error rates stay below 5% for 95% sequences, outperforming naive self-normalized methods that can exceed 20% false positives.

These results matter because they enable safe, flexible experimentation amid streaming data, reducing costs from erroneous decisions in high-stakes settings like product launches or policy trials. Unlike prior work limited to parametric or finite horizons, these sequences generalize to martingales (cumulative processes) and support continuous monitoring without approximations, cutting Type I errors that plague "p-hacking." They align with real-world needs, where experiments rarely follow rigid plans, and offer tighter constants than existing nonparametric bounds—potentially halving effective widths in practice.

Leaders should integrate these sequences into A/B testing platforms for ongoing monitoring, starting with the closed-form stitched or mixture bounds for sub-Gaussian data like bounded metrics. For causal studies, adopt the empirical-Bernstein version in potential outcomes models to estimate treatment effects sequentially. Trade-offs include choosing mixture boundaries for short-to-medium runs (up to three orders of magnitude in sample size) versus stitched ones for theoretical guarantees. Further work is needed: pilot implementations in software like R or Python, more benchmarks against group-sequential methods for batched data, and extensions to anticoncentration bounds for lower tails.

Limitations include wider intervals than asymptotic fixed-sample methods (by a factor under 2 for practical sizes) and reliance on tail conditions like sub-Gaussianity, which may not hold for very heavy tails without adjustments. Confidence is strong in the derivations, proven nonasymptotically, and simulations validate coverage across diverse cases; caution is advised for non-independent data or when variance explodes, where additional validation data would help.

1. Introduction

Section Summary: Organizations commonly run large-scale A/B tests to enhance online products and user experiences, but these experiments unfold sequentially as data streams in, and traditional analysis methods that assume a fixed sample size often inflate error rates by monitoring results continuously. This paper introduces confidence sequences, which are evolving confidence intervals that provide reliable coverage for key parameters at every step, allowing experimenters to stop or continue flexibly without compromising validity. These tools draw from established statistical frameworks, work in diverse scenarios, and offer stronger guarantees than standard approaches, though they result in slightly wider intervals to account for uncertainty over time.

It has become standard practice for organizations with online presence to run large-scale randomized experiments, or "A/B tests", to improve product performance and user experience. Such experiments are inherently sequential: visitors arrive in a stream and outcomes are typically observed quickly relative to the duration of the test. Results are often monitored continuously using inferential methods that assume a fixed sample, despite the known problem that such monitoring inflates Type I error substantially ([1, 2]). Furthermore, most A/B tests are run with little formal planning and fluid decision-making, compared to clinical trials or industrial quality control, the traditional applications of sequential analysis.

This paper presents methods for deriving confidence sequences as a flexible tool for inference in sequential experiments ([3, 4, 5]). For $\alpha \in (0, 1)$, a $(1-\alpha)$-confidence sequence is a sequence of confidence sets $(\textup{CI}t){t=1}^\infty$, typically intervals $\textup{CI}_t = (L_t, U_t) \subseteq \mathbb{R}$, satisfying a uniform coverage guarantee: after observing the $t$ $^{\text{th}}$ unit, we calculate an updated confidence set $\textup{CI}_t$ for the unknown quantity of interest $\theta_t$, with the uniform coverage property

$ \begin{align} \mathbb{P}(\forall t \geq 1 : \theta_t \in \textup{CI}_t) \geq 1 - \alpha. \end{align}\tag{1} $

With only a uniform lower bound $(L_t)$, i.e., if $U_t \equiv \infty$, we have a lower confidence sequence. Likewise, if $L_t \equiv -\infty$ we have an upper confidence sequence given by $(U_t)$. Theorem 5, Theorem 9, and Theorem 10 and Lemma 7 are our key tools for constructing confidence sequences. All build upon the general framework for uniform exponential concentration introduced in [6], which means our techniques apply in diverse settings: scalar, matrix, and Banach-space-valued observations, with possibly unbounded support; self-normalized bounds applicable to observations satisfying weak moment or symmetry conditions; and continuous-time scalar martingales. Our methods allow for flexible control of the "shape" of the confidence sequence, that is, how the sequence of intervals shrinks in width over time. As a simple example, given a sequence of i.i.d.\ observations $(X_t)_{t=1}^\infty$ from a 1-sub-Gaussian distribution whose mean $\mu$ we would like to estimate, Theorem 5 yields the following $(1-\alpha)$-confidence sequence for $\mu$, a special case of the more general bound Equation 6:

$ \begin{align} \frac{\sum_{i=1}^t X_i}{t} \pm 1.7 \sqrt{\frac{\log \log(2t) + 0.72 \log(10.4 / \alpha)}{t}}. \end{align}\tag{2} $

The $\mathcal{O}(\sqrt{t^{-1} \log \log t})$ asymptotic rate of this bound matches the lower bound implied by the law of the iterated logarithm (LIL), and nonasymptotic bounds of this form are called finite LIL bounds ([7]).

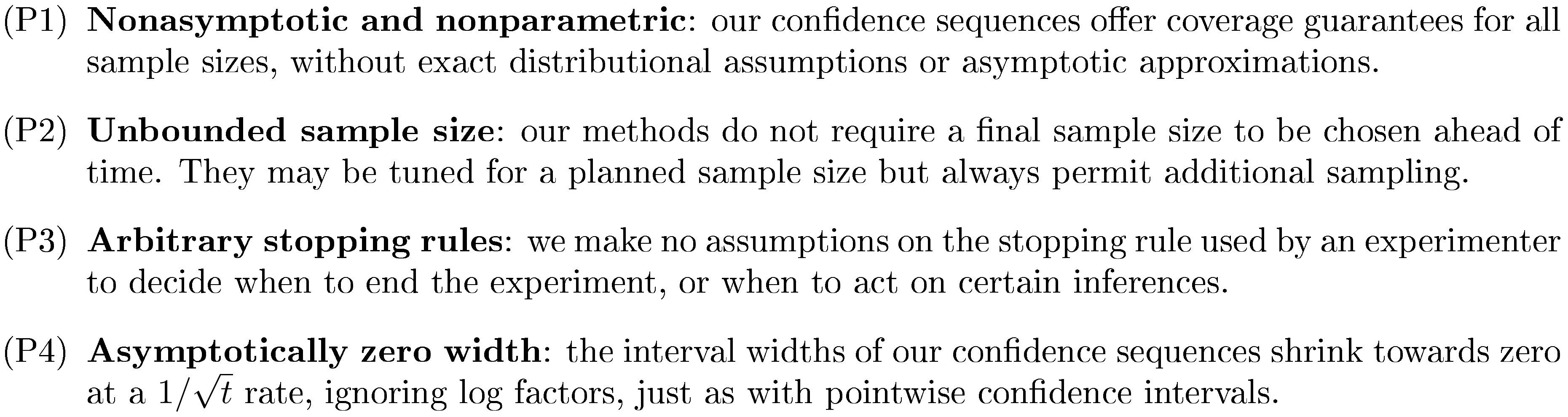

We develop confidence sequences that possess the following properties:

These properties give us strong guarantees and broad applicability. An experimenter may always choose to gather more samples, and may stop at any time according to any rule—the resulting inferential guarantees hold under the stated assumptions without any approximations. Of course, this flexibility comes with a cost: our intervals are wider than those that rely on asymptotics or make stronger assumptions, for example, a known stopping rule. Typical, fixed-sample confidence intervals derived from the central limit theorem do not satisfy any of (P1)-(P3), and accommodating any one property necessitates wider intervals; we illustrate this in Figure 1. It is perhaps surprising that these four properties come at a numerical cost of less than doubling the fixed-sample, asymptotic interval width—the discrete mixture bound illustrated in Figure 9 stays within a factor of two of the fixed-sample CLT bounds over five orders of magnitude in time.

1.1 Related work

The idea of a confidence sequence goes back at least to [3]. They are called repeated confidence intervals by [8, 5] (with a focus on finite time horizons) and always-valid confidence intervals by [9]. They are sometimes labeled anytime confidence intervals in the machine learning literature ([10]).

Prior work on sequential inference is often phrased in terms of a sequential hypothesis test, defined as a stopping rule and an accept/reject decision variable, or in terms of an always-valid $p$-value ([9]). In Section 6 we discuss the duality between confidence sequences, sequential hypothesis tests, and always-valid $p$-values. We show in Lemma 19 that definition Equation 1 is equivalent to requiring $\mathbb{P}(\theta_\tau \in \textup{CI}_\tau) \geq 1 - \alpha$ for all stopping times $\tau$, or even for all random times $\tau$, not necessarily stopping times. Hence the choice of definition Equation 1 over related definitions in the literature is one of convenience.

Recent interest in confidence sequences has come from the literature on best-arm identification with fixed confidence for multi-armed bandit problems. [11], [7], [12], and [13] present methods satisfying properties (P1)-(P4) for independent, sub-Gaussian observations. Our results are sharper and more general, and our Bernstein confidence sequence scales with the true variance in nonparametric settings. Confidence sequences are a key ingredient in best-arm selection algorithms ([14]) and related methods for sequential testing with multiple comparisons ([15, 16, 10]). Our results improve and generalize such methods.

[17] and [18] prove empirical-Bernstein bounds for fixed times or finite time horizons. Our empirical-Bernstein bound holds uniformly over infinite time. [19] takes a different approach to deriving confidence sequences satisfying properties (P1)-(P4) by lower bounding a mixture martingale. This work was extended in [20] to an empirical-Bernstein bound, the only infinite-horizon, empirical-Bernstein confidence sequence we are aware of in prior work. Our result removes a multiplicative pre-factor and yields sharper bounds. We emphasize that our proof technique is quite different from all three of these existing empirical-Bernstein bounds; see Appendix A.8.

The simplest confidence sequence satisfying properties (P1)-(P3) follows by inverting a suitably formulated sequential probability ratio test (SPRT, ([21])), such as in Section 3.6 of [6]. Wald worked in a parametric setting, though it is known that the normal SPRT depends only on sub-Gaussianity (e.g., [22]). The resulting confidence sequence does not shrink towards zero width as $t \to \infty$ (property P4), a problem which stems from the choice of a single point alternative $\lambda$. Numerous extensions have been developed to remedy this defect, and our work is most closely tied to two approaches. First, in the method of mixtures, one replaces the likelihood ratio with a mixture $\int \prod_i [f_\lambda(X_i) / f_0(X_i)] \mathop{}!\mathrm{d} F(\lambda)$, which is still a martingale ([23, 21, 24, 25, 26, 22, 27, 28, 19, 29, 30]). Second, epoch-based analyses choose a sequence of point alternatives $\lambda_1, \lambda_2, \dots$ approaching the null value, with corresponding error probabilities $\alpha_1, \alpha_2, \dots$ approaching zero so that a union bound yields the desired error control ([31, 32, 12]).

The literature on self-normalized bounds makes extensive use of the method of mixtures, sometimes called pseudo-maximization ([33, 28, 34, 35, 11]); these works introduced the idea of using a mixture to bound a quantity with a random intrinsic time $V_t$. These results are mostly given for fixed samples or finite time horizon, though [33], Eq. 4.20 includes an infinite-horizon curve-crossing bound. [27] treats confidence sequences for the parameter of an exponential family using mixture techniques similar to those of Section 3.2. Like most work on the method of mixtures, Lai's work focused on the parametric setting (which we discuss in Section 4.4), while we focus on the application of mixture bounds to nonparametric settings.

[36] adopt the mixture approach for a commercial A/B testing platform, where properties (P2) and (P3) are critical to provide an "off-the-shelf" solution for a variety of clients. Their application relies on asymptotics which lack rigorous justification. In Section 4.2 we give nonasymptotic justification for a similar confidence sequence under a finite-sample randomization inference model, and in Section 5 we demonstrate how our methods control Type I error in situations where asymptotics fail.

1.2 Outline

We organize our results using the sub-Gaussian, sub-gamma, sub-Bernoulli, sub-Poisson and sub-exponential settings defined in Section 2.

- The stitching method gives new closed-form sub-Gaussian or sub-gamma boundaries (Theorem 5). Our sub-gamma treatment extends prior sub-Gaussian work to cover any martingale whose increments have finite moment-generating function in a neighborhood of zero; see Proposition 3. Our proof is transparent and flexible, accommodating a variety of boundary shapes, including those growing at the rate $\mathcal{O}(\sqrt{t \log \log t})$ with a focus on tight constants, though we do not recommend this bound in practice unless closed-form simplicity is vital.

- Conjugate mixtures give one- and two-sided boundaries for the sub-Bernoulli, sub-Gaussian, sub-Poisson and sub-exponential cases (Section 3.2) which avoid approximations made for analytical convenience. The sub-Gaussian boundaries are unimprovable without further assumptions (Section 3.6). These boundaries include a common tuning parameter which is critical in practice and we discuss why their $\mathcal{O}(\sqrt{t \log t})$ growth rate may be preferable to the slower $\mathcal{O}(\sqrt{t \log \log t})$ rate (Section 3.5).

- Discrete mixtures facilitate numerical computation of boundaries with a great deal of flexibility, at the cost of slightly more involved computations (Theorem 9). Like conjugate mixture boundaries, these boundaries avoid unnecessary approximations and are unimprovable in the sub-Gaussian case.

- Finally, for sub-Gaussian processes, the inverted stitching method (Theorem 10) gives numerical upper bounds on the crossing probability of any increasing, strictly concave boundary over a limited time range. We show that any such boundary yields a uniform upper tail inequality over a finite horizon, and compute its crossing probability.

Building on this foundation, we present a a state-of-the-art empirical-Bernstein bound (Theorem 13) for any sequence of bounded observations using a new self-normalization proof technique. We illustrate our methods with two novel applications: the nonasymptotic, sequential estimation of average treatment effect in the Neyman-Rubin potential outcomes model (Section 4.2), and the derivation of uniform matrix bounds and covariance matrix confidence sequences (Corollary 15 and Section 4.3). We give simulation results in Section 5. Section 6 discusses the relationship of our work to existing concepts of sequential testing. Proofs of main results are in Appendix A, with others deferred to Appendix C.

2. Preliminaries: linear boundaries

Section Summary: This section explains how to estimate the average expected value of a sequence of observations over time using a running sample mean, while accounting for deviations from those expectations through a process called S_t. To create reliable lower bounds for these estimates—known as confidence sequences—it focuses on uniform upper tail probabilities for S_t, scaled by an "intrinsic time" process V_t that tracks squared deviations, without assuming the observations are independent or have the same mean. The approach builds on a mathematical condition called the sub-ψ property, rooted in martingale techniques from probability theory, which ensures the exponential growth of deviations can be controlled like a supermartingale to derive these bounds.

Given a sequence of real-valued observations $(X_t){t=1}^\infty$, suppose we wish to estimate the average conditional expectation $\mu_t \coloneqq t^{-1} \sum{i=1}^t \mathbb{E}{i-1} X_i$ at each time $t$ using the sample mean $\bar{X}t \coloneqq t^{-1} \sum{i=1}^t X_i$; here we assume an underlying filtration $(\mathcal{F}t){t=1}^\infty$ to which $(X_t)$ is adapted, and $\mathbb{E}t$ denotes expectation conditional on $\mathcal{F}t$. Let $S_t \coloneqq \sum{i=1}^t (X_i - \mathbb{E}{i-1} X_i)$, the zero-mean deviation of our sample sum from its estimand at time $t$. Given $\alpha \in (0, 1)$, suppose we can construct a uniform upper tail bound $u\alpha: \mathbb{R}{\geq 0} \to \mathbb{R}{\geq 0}$ satisfying

$ \begin{align} \mathbb{P}\big(\exists t \geq 1 : S_t \geq u_\alpha(V_t)\big) \leq \alpha \end{align}\tag{3} $

for some adapted, real-valued intrinsic time process $(V_t){t=1}^\infty$, an appropriate time scale to measure the (squared) deviations of $(S_t)$. This uniform upper bound on the centered sum $(S_t)$ yields a lower confidence sequence for $(\mu_t)$ with radius $t^{-1} u\alpha(V_t)$: $\mathbb{P}\left(\forall t \geq 1 : \bar{X}t - t^{-1} u\alpha(V_t) \leq \mu_t \right) \geq 1 - \alpha$.

Note that an assumption on the upper tail of $(S_t)$ yields a lower confidence sequence for $(\mu_t)$; a corresponding assumption on the lower tail of $(S_t)$ yields an upper confidence sequence for $(\mu_t)$. In this paper we formally focus on upper tail bounds, from which lower tail bounds can be derived by examining $(-S_t)$ in place of $(S_t)$. In general, the left and right tails of $(S_t)$ may behave differently and require different sets of assumptions, so that our upper and lower confidence sequences may have different forms. Regardless, we can always combine upper and lower confidence sequences using a union bound to obtain a two-sided confidence sequence Equation 1.

When the $(X_t)$ are independent with common mean $\mu$, the resulting confidence sequence estimates $\mu$, but the setup requires neither independence nor a common mean. In general, the estimand $\mu_t$ may be changing at each time $t$; Section 4.2 gives an application to causal inference in which this changing estimand is useful. In principle, $\mu_t$ may also be random, although none of our applications involve random $\mu_t$.

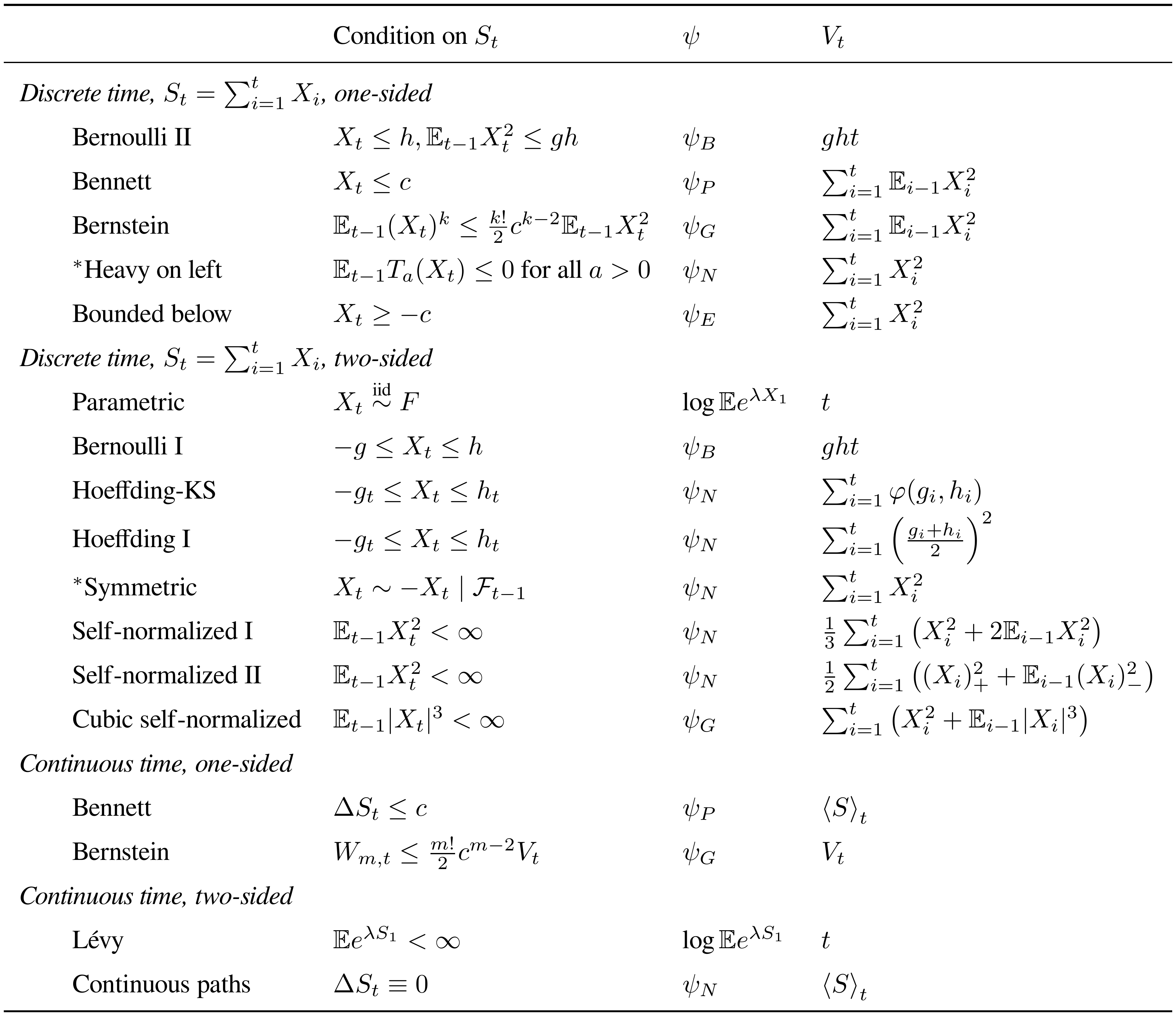

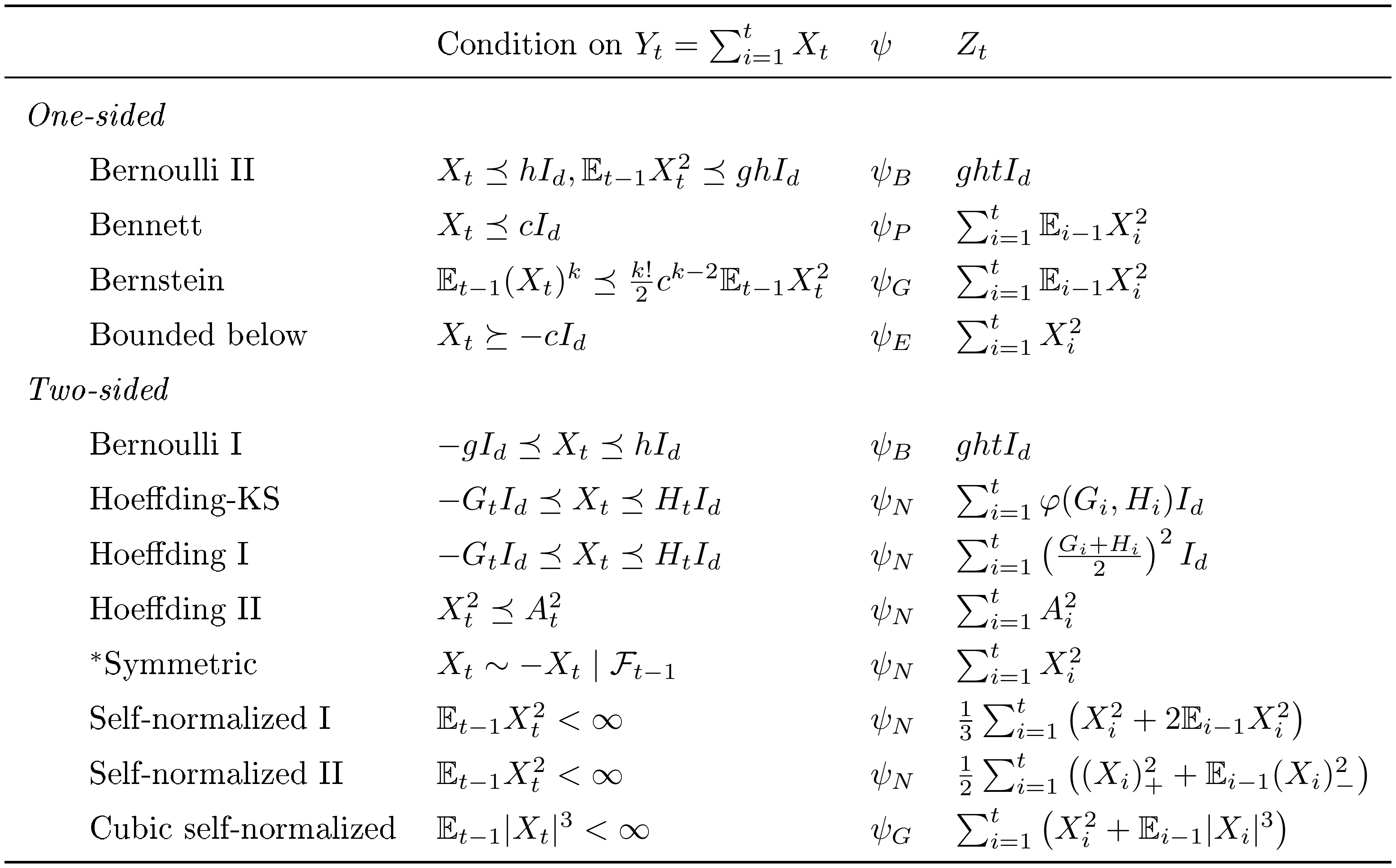

To construct uniform boundaries $u_\alpha$ satisfying inequality Equation 3, we build upon the following general condition ([6], Definition 1):

########## {caption="Definition 1: Sub- $\psi$ condition"}

Let $\smash{(S_t){t = 0}^\infty, (V_t){t = 0}^\infty}$ be real-valued processes adapted to an underlying filtration $(\mathcal{F}t){t = 0}^\infty$ with $\smash{S_0=V_0=0}$ and $\smash{V_t\geq0}$ for all $t$. For a function $\psi: [0, \lambda_{\max}) \to \mathbb{R}$ and a scalar $l_0 \in [1, \infty)$, we say $(S_t)$ is $l_0$-sub- $\psi$ with variance process $(V_t)$ if, for each $\lambda \in [0, \lambda_{\max})$, there exists a supermartingale $(L_t(\lambda))_{t = 0}^\infty$ w.r.t. $(\mathcal{F}_t)$ such that $\mathbb{E} L_0(\lambda) \leq l_0$ and

$ \begin{align} \exp \left\lbrace \lambda S_t - \psi(\lambda) V_t \right\rbrace \leq L_t(\lambda) \text{ a.s.\ for all } t. \end{align} $

For given $\psi$ and $l_0$, let $\mathbb{S}^{l_0}_{\psi}$ be the class of pairs of $l_0$-sub- $\psi$ processes $(S_t, V_t)$:

$ \begin{align} \mathbb{S}^{l_0}_{\psi} \coloneqq \left\lbrace (S_t, V_t): (S_t) \text{ is $l_0$-sub-$\psi$ with variance process } (V_t) \right\rbrace. \end{align} $

When stating that a process is sub- $\psi$, we typically omit $l_0$ from our terminology for simplicity. In scalar cases, we always have $l_0 = 1$, while in matrix cases $l_0 = d$, the dimension of the (square) matrices.

Where does Definition 1 come from? The jumping-off point is the martingale method for concentration inequalities (([37, 38, 39]); ([40], section 2.2)), itself based on the classical Cramér-Chernoff method (([41, 42]); ([43], section 2.2)). The martingale method starts off with an assumption of the form $\mathbb{E}{t-1}e^{\lambda(X_t - \mathbb{E}{t-1} X_t)}\leq e^{\psi(\lambda)\sigma_t^2}$ for all $t \geq 1, \lambda \in \mathbb{R}$. Then, denoting $S_t \coloneqq \sum_{i=1}^t (X_i - \mathbb{E}{i-1} X_i)$ and $V_t \coloneqq \sum{i=1}^t \sigma_i^2$, the process $\exp \left\lbrace \lambda S_t - \psi(\lambda) V_t \right\rbrace$ is a supermartingale for each $\lambda \in \mathbb{R}$. Unlike the martingale method assumption, Definition 1 allows the exponential process to be upper bounded by a supermartingale, and it permits $(V_t)$ to be adapted rather than predictable. We also restrict our attention to $\lambda \geq 0$ to derive one-sided bounds.

Intuitively, the process $\exp \left\lbrace \lambda S_t - \psi(\lambda) V_t \right\rbrace$ measures how quickly $S_t$ has grown relative to intrinsic time $V_t$, and the free parameter $\lambda$ determines the relative emphasis placed on the tails of the distribution of $S_t$, i.e., on the higher moments. Larger values of $\lambda$ exaggerate larger movements in $S_t$, and $\psi$ captures how much we must correspondingly exaggerate $V_t$. $\psi$ is related to the heavy-tailedness of $S_t$ and the reader may think of it as a cumulant-generating function (CGF, the logarithm of the moment-generating function). For example, suppose $(X_t)$ is a sequence of i.i.d., zero-mean random variables with CGF $\psi(\lambda) \coloneqq \log \mathbb{E} e^{\lambda X_1}$ which is finite for all $\lambda \in [0, \lambda_{\max})$. Then, setting $V_t \coloneqq t$, we see that $L_t(\lambda) \coloneqq \exp \left\lbrace \lambda S_t - \psi(\lambda) V_t \right\rbrace$ is itself a martingale, for all $\lambda \in [0, \lambda_{\max})$. Indeed, in all scalar cases we consider, $L_t(\lambda)$ is just equal to $\exp \left\lbrace \lambda S_t - \psi(\lambda) V_t \right\rbrace$. See Appendix Table 3 and Table 4, drawn from [6], for a catalog of sufficient conditions for a process to be sub- $\psi$ using the five $\psi$ functions defined below. We use many of these conditions in what follows.

We organize our uniform boundaries according to the $\psi$ function used in Definition 1. First recall the Cramér-Chernoff bound: if $(X_t)$ are independent zero-mean with bounded CGF $\log \mathbb{E} e^{\lambda X_t} \leq \psi(\lambda)$ for all $t \geq 1$ and $\lambda \in \mathbb{R}$, then writing $S_t = \sum_{i=1}^t X_i$, we have $\mathbb{P}(S_t \geq x) \leq e^{-t \psi^\star(x/t)}$ for any $x > 0$, where $\psi^\star$ denotes the Legendre-Fenchel transform of $\psi$. Equivalently, writing $z_\alpha(t) \coloneqq t {\psi^\star}^{-1}(t^{-1} \log \alpha^{-1})$, we have $\mathbb{P}(S_t \geq z_\alpha(t)) \leq \alpha$ for any fixed $t$ and $\alpha \in (0, 1)$. In other words, the function $z_\alpha$ gives a high-probability upper bound at any fixed time $t$ for any sum of independent random variables with CGF bounded by $\psi$. When we extend this concept to boundaries holding uniformly over time, there is no longer a unique, minimized boundary, and the following definition captures the class of valid boundaries.

########## {caption="Definition 2"}

Given $\smash{\psi: [0, \lambda_{\max}) \to \mathbb{R}}$ and $\smash{l_0\geq 1}$, a function $\smash{u: \mathbb{R}\to \mathbb{R}}$ is called an $l_0$-sub- $\psi$ uniform boundary with crossing probability $\alpha$ if

$ \begin{align} \sup_{(S_t, V_t) \in \mathbb{S}^{l_0}_{\psi}} \mathbb{P}(\exists t \geq 1: S_t \geq u(V_t)) \leq \alpha. \end{align} $

Although $u$ does depend on the constant $l_0$ in Definition 1, for simplicity we typically omit this dependence from our notation, writing simply that $u$ is a sub- $\psi$ uniform boundary.

Five particular $\psi$ functions play important roles in our development; below, we take $1 / 0 = \infty$ in the upper bounds on $\lambda$:

- $\psi_{B, g, h}(\lambda) \coloneqq \frac{1}{gh} \log\left(\frac{ge^{h\lambda} + he^{-g\lambda}}{g+h} \right)$ on $0 \leq \lambda < \infty$, the scaled CGF of a centered random variable (r.v.) supported on two points, $-g$ and $h$, for some $g, h > 0$, for example a centered Bernoulli r.v. when $g + h = 1$.

- $\psi_N(\lambda) \coloneqq \lambda^2/2$ on $0 \leq \lambda < \infty$, the CGF of a standard Gaussian r.v.

- $\psi_{P, c}(\lambda) \coloneqq c^{-2}(e^{c\lambda} - c\lambda - 1)$ on $0 \leq \lambda < \infty$ for some scale parameter $c \in \mathbb{R}$, which is the CGF of a centered unit-rate Poisson r.v. when $c=1$. By taking the limit, we define $\psi_{P, 0} = \psi_N$.

- $\psi_{E, c}(\lambda) \coloneqq c^{-2}(-\log(1-c\lambda) - c\lambda)$ on $0 \leq \lambda < 1 / (c \vee 0)$ for some scale $c \in \mathbb{R}$, which is the CGF of a centered unit-rate exponential r.v. when $c = 1$. By taking the limit, we define $\psi_{E, 0} = \psi_N$.

- $\psi_{G, c}(\lambda) \coloneqq \lambda^2 / (2 (1 - c\lambda))$ on $0 \leq \lambda < 1 / (c \vee 0)$ (taking $1/0 = \infty$) for some scale parameter $c \in \mathbb{R}$, which we refer to as the sub-gamma case following [43]. This is not the CGF of a gamma r.v. but is a convenient upper bound which also includes the sub-Gaussian case at $c = 0$ and permits analytically tractable results below.

One may freely scale $\psi$ by any positive constant and divide $V_t$ by the same constant so that Definition 1 remains satisfied; by convention, we scale all $\psi$ functions above so that $\psi''(0_+) = 1$. When we speak of a sub-gamma process (or uniform boundary) with scale parameter $c$, we mean a sub- $\psi_{G, c}$ process (or uniform boundary), and likewise for other cases. We often write $\psi_B$, $\psi_P$, etc., dropping the range and scale parameters from our notation. As we summarize in Figure 2 and detail in Proposition 31, certain general implications hold among sub- $\psi$ boundaries. In particular, any sub-Gaussian boundary can also serve as a sub-Bernoulli boundary; any sub-Poisson boundary serves as a sub-Gaussian or sub-Bernoulli boundary; and, importantly, any sub-gamma or sub-exponential boundary can serve as a sub- $\psi$ boundary in any of the other four cases. Indeed, a sub-gamma or sub-exponential boundary applies to many cases of practical interest, as detailed below.

########## {caption="Proposition 3"}

Suppose $\psi$ is twice-differentiable and $\smash{\psi(0) = \psi'(0_+) = 0}$. Suppose, for each $c>0$, $u_c(v)$ is a sub-gamma or sub-exponential uniform boundary with crossing probability $\alpha$ for scale $c$. Then $v \mapsto u_{k_1}(k_2v)$ is a sub- $\psi$ uniform boundary for some constants $k_1, k_2 > 0$ depending only on $\psi$.

Proposition 3 restates [6], Proposition 1, which shows that any process $(S_t)$ which is sub- $\psi$ is also sub-gamma and sub-exponential, if $\psi$ satisfies the conditions of Proposition 3. Note that these conditions are satisfied for any mean-zero random variable if the CGF exists in a neighborhood of zero, so the conditions are quite weak ([44], Theorem 2.3).

########## {#thm:ex_variance caption="Confidence sequence for the variance of a Gaussian distribution

with unknown mean" type="Example"

Suppose $X_1, X_2, \dots$ are i.i.d.\ draws from a $\mathcal{N}(\mu, \sigma^2)$ distribution and we wish to sequentially estimate $\sigma^2$ when $\mu$ is also unknown. Let $S_t \coloneqq \sigma^{-2} \sum_{i=1}^{t+1} (X_i - \bar{X}{t+1})^2 - t$ for $t = 1, 2, \dots$, where $\bar{X}t \coloneqq t^{-1} \sum{i=1}^t X_i$ is the sample mean. This $S_t$ is a centered and scaled sample variance, and as in [3], we use the fact that $S_t$ is a cumulative sum of independent, centered Chi-squared random variables each with one degree of freedom (see Appendix H for details). Such a centered Chi-squared distribution has variance two and CGF equal to $2 \psi{E, 2}$.

Thus $(S_t)$ is 1-sub-exponential with variance process $V_t = 2t$ and scale parameter $c = 2$. We may uniformly bound the upper deviations of $S_t$ using any sub-exponential uniform boundary, for example the gamma-exponential mixture boundary of Proposition 24. Or, we can use Proposition 31 to deduce that $(S_t)$ is sub-gamma with scale $c = 2$ (and the same variance process) and use the closed-form stitched boundary of Theorem 5.

The above constructions yield lower confidence sequences for the variance. To obtain an upper confidence sequence, we use the fact that $(-S_t)$ is 1-sub-exponential with scale parameter $\smash{c = -2}$. Now Proposition 31 implies that $(-S_t)$ is sub-gamma with scale $c = -1$, so the stitched boundary again applies, while Proposition 31 implies that $(-S_t)$ is also sub-Gaussian, so we may alternatively use the normal mixture boundary of Proposition 21. Since $\psi_{G, -1}$ is uniformly smaller than $\psi_N$, the above analysis yields tighter bounds than the sub-Gaussian approach of [3].

The simplest uniform boundaries are linear with positive intercept and slope. This is formalized in [6], partially restated below.

########## {caption="Lemma 4: ([6]), Theorem 1"}

For any $\lambda \in [0, \lambda_{\max})$ and $\alpha \in (0, 1)$,

$ \begin{align} u(v) \coloneqq \frac{\log(l_0 / \alpha)}{\lambda}

- \frac{\psi(\lambda)}{\lambda} \cdot v \end{align} $

is a sub- $\psi$ uniform boundary with crossing probability $\alpha$.

While Lemma 4 provides a versatile building block, the $\mathcal{O}(V_t)$ growth of $u(V_t)$ may be undesirable. Indeed, from a concentration point of view, the typical deviations of $S_t$ tend to be only $\mathcal{O}(\sqrt{V_t})$, so the bound will rapidly become loose for large $t$. From a confidence sequence point of view, recall that the confidence radius for the mean is given by $u(V_t) / t$. Typically, $V_t = \Theta(t)$ a.s. as $t \to \infty$, so the confidence radius will be asymptotically zero width if and only if $u(v) = o(v)$. In other words, we cannot achieve arbitrary estimation precision with arbitrarily large samples unless the uniform boundary is sublinear. We address this problem in Section 3, building upon Lemma 4 to construct curved sub- $\psi$ uniform boundaries.

3. Curved uniform boundaries

Section Summary: This section outlines techniques for computing curved uniform boundaries to control the excursions of random processes, such as sub-Gaussian or sub-gamma ones, which are useful in fields like statistics and machine learning. It focuses on a "stitched" analytical boundary that combines simpler linear bounds across geometrically spaced time periods, requiring user-chosen parameters to set the starting point, growth rate, and overall shape. The method guarantees that the probability of the process crossing this boundary remains below a specified small value, with growth behaving like the square root of time multiplied by the log of log time in key examples, ensuring reliable performance through careful tuning.

We present our four methods for computing curved uniform boundaries in Figure 3, Section 3.2, Figure 8, and Section 3.4. In Section 3.5, we discuss how to tune boundaries, a necessity for good performance in practice, and we describe the unimprovability of sub-Gaussian mixture bounds in Section 3.6.

3.1 Closed-form boundaries via stitching

Our analytical "stitched" bound is useful in the sub-Gaussian case or, more generally, the sub-gamma case with scale $c$. We require three user-chosen parameters:

- a scalar $\eta > 1$ determines the geometric spacing of intrinsic time,

- a scalar $m > 0$ which gives the intrinsic time at which the uniform boundary starts to be nontrivial, and

- an increasing function $h : \mathbb{R}{\geq 0} \to \mathbb{R}{>0}$ such that ${\sum_{k=0}^\infty 1 / h(k) \leq 1}$, which determines the shape of the boundary's growth after time $m$.

Recalling the scale parameter $c$ for the $\psi_G$ function above and the constant $l_0$ in Definition 1, we define the stitching function $\mathcal{S}_\alpha$ as

$ \mathcal{S}_\alpha(v) \coloneqq \sqrt{k_1^2 v \ell(v) + k_2^2 c^2 \ell^2(v)} \

- k_2 c \ell(v), \text{ where } \begin{cases} \ell(v) \coloneqq \log h(\log_{\eta}(\frac{v}{m})) + \log(\frac{l_0}{\alpha}), \ k_1 \coloneqq (\eta^{1/4} + \eta^{-1/4}) / \sqrt{2}, \ k_2 \coloneqq (\sqrt{\eta} + 1) / 2, \end{cases}\tag{4} $

and define the stitched boundary as $u(v) = \mathcal{S}\alpha(v \vee m)$. Note $\mathcal{S}\alpha(v) \leq k_1 \sqrt{v \ell(v)} + 2 c k_2 \ell(v)$ when $c > 0$, while $\mathcal{S}\alpha(v) \leq k_1 \sqrt{v \ell(v)}$ when $c \leq 0$, with equality in the sub-Gaussian case ($c = 0$). These simpler expressions may sometimes be preferable. For notational simplicity we suppress the dependence of $\mathcal{S}\alpha$ on $h$, $\eta$, $l_0$, and $c$; we will discuss specific choices as necessary. In the examples we consider, $\ell(v)$ grows as $\mathcal{O}(\log v)$ or $\mathcal{O}(\log \log v)$ as $v \uparrow \infty$, so the first term, $k_1 \sqrt{V_t \ell(V_t)}$, dominates for sufficiently large $V_t$, specifically when $V_t / \ell(V_t) \gg 2c^2\sqrt{\eta}$.

########## {caption="Theorem 5: Stitched boundary"}

For any $\smash{c \geq 0, \alpha \in (0, 1), \eta > 1, m>0}$, and $\smash{h : \mathbb{R}{\geq 0} \to \mathbb{R}{\geq 0}}$ increasing such that $\smash{\sum_{k=0}^\infty 1 / h(k) \leq 1}$, the function $v \mapsto \mathcal{S}_\alpha(v \vee m)$ is a sub-gamma uniform boundary with crossing probability $\alpha$. Further, for any sub- $\psi_G$ process $(S_t)$ with variance process $(V_t)$ and any $v_0 \geq m$,

$ \begin{align} \mathbb{P}\left(\exists t \geq 1: V_t \geq v_0 \text{ and } S_t \geq \mathcal{S}\alpha(V_t) \right) \leq \sum{k=\lfloor \log_\eta(v_0/m) \rfloor}^\infty \frac{\alpha}{h(k)}. \end{align}\tag{5} $

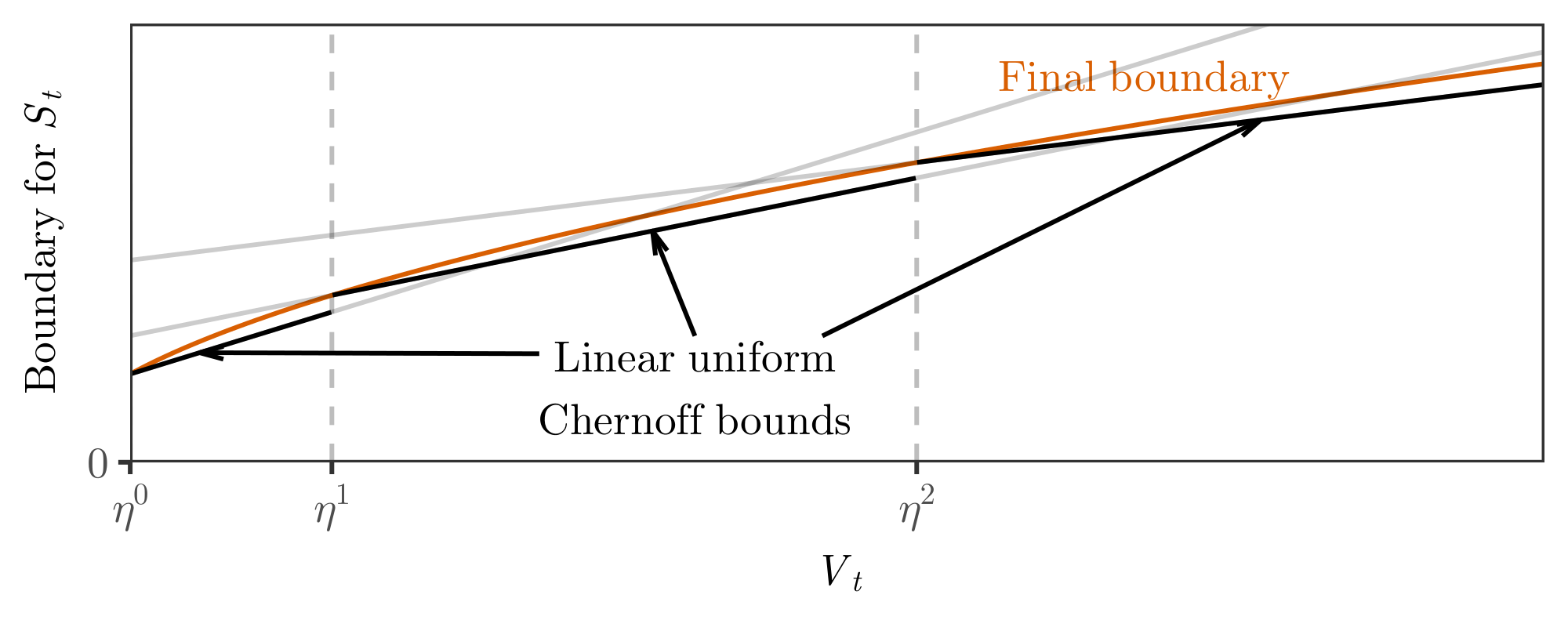

The first sentence above says that the probability of $S_t$ crossing $\mathcal{S}\alpha(V_t \vee m)$ at least once is at most $\alpha$, while the second says that, even if it does happen to cross once or more, the probability of further crossings decays to zero beyond larger and larger intrinsic times $v_0$. Note that Equation 5 implies $\mathbb{P}\left(\sup_t V_t = \infty and S_t \geq \mathcal{S}\alpha(V_t) infinitely often \right) = 0$. The proof of Theorem 5, given with discussion in Appendix A.1, follows by taking a union bound over a carefully chosen family of linear boundaries, one for each of a sequence of geometrically-spaced epochs; see Figure 3. The high-level proof technique is standard, often referred to as "peeling" in the bandit literature, and closely related to chaining elsewhere in probability theory. Our proof generalizes beyond the sub-Gaussian case and involves careful parameter choices in order to achieve tight constants. In brief, within each epoch, there are many possible linear boundaries, and we have found that optimizing the linear boundary for the geometric mean of the epoch endpoints strikes a good balance between tight constants and analytical simplicity in the final boundary. Appendix G gives a detailed comparison of constants arising from our bound with similar bounds from the literature.

The boundary shape is determined by choosing the function $h$ and setting the nominal crossing probability in the $k$ $^{\text{th}}$ epoch to equal $\alpha/h(k)$. Then Theorem 5 gives a curved boundary which grows at a rate $\mathcal{O}\left(\sqrt{V_t \log h(\log_\eta V_t)} \right)$ as $V_t \uparrow \infty$. The more slowly $h(k)$ grows as $k \uparrow \infty$, the more slowly the resulting boundary will grow as $V_t \uparrow \infty$. A simple choice is exponential growth, $h(k) = \eta^{sk} / (1 - \eta^{-s})$ for some $s > 1$, yielding $\mathcal{S}_\alpha(v) = \mathcal{O}(\sqrt{v \log v})$. A more interesting example is $h(k) = (k + 1)^s \zeta(s)$ for some $s > 1$, where $\zeta(s)$ is the Riemann zeta function. Then, when $l_0 = 1$, Theorem 5 yields the polynomial stitched boundary: for $c \geq 0$,

$ \begin{align} \mathcal{S}_\alpha(v) = k_1 \sqrt{ v \left(s \log\log\left(\frac{\eta v}{m} \right)

- \log \frac{\zeta(s)}{\alpha \log^s \eta} \right) }

- c k_2 \left(s \log\log\left(\frac{\eta v}{m} \right)

- \log \frac{\zeta(s)}{\alpha \log^s \eta} \right), \end{align}\tag{6} $

where the second term is neglected in the sub-Gaussian case since $c=0$. This is a "finite LIL bound", so-called because $\mathcal{S}_\alpha(v) \sim \sqrt{s k_1^2 v \log \log v}$, matching the form of the law of the iterated logarithm ([45]). We can bring $s k_1^2$ arbitrarily close to $2$ by choosing $\eta$ and $s$ sufficiently close to one, at the cost of inflating the additive term $\log(\zeta(s) / (\log^s \eta))$. Briefly, increasing $\eta$ increases the size of each epoch in the aforementioned peeling argument, which reduces the looseness of the union bound over epochs. But the larger we make the epochs, the further each linear boundary deviates from the ideal curved shape at the ends of the epochs, which inflates our final boundary. The choice of $s$ involves a similar tradeoff: increasing $s$ causes us to exhaust more of our total error probability budget on earlier epochs, decreasing the constant term (which matters most for early times), at the cost of a union bound over smaller error probabilities in later epochs, which shows up as an increase in the leading constant. We discuss parameter tuning in more practical terms in Section 3.5. For example, take $\smash{\eta = 2, s = 1.4, m = 1}$; if $S_t$ is a sum of independent, zero-mean, 1-sub-Gaussian observations, we obtain

$ \begin{align} \mathbb{P}\left(\exists t \geq 1 : S_t \geq 1.7 \sqrt{t \left(\log \log(2t) + 0.72 \log \left(\frac{5.2}{\alpha} \right) \right)} \right) \leq \alpha. \end{align}\tag{7} $

Figure 9 in Appendix G compares a sub-Gaussian stitched boundary to a numerically-computed discrete mixture bound with a mixture distribution roughly corresponding to $h(k) \propto (k+1)^{1.4}$, as described in Appendix A.6. This discrete mixture boundary acts as a lower bound (see Section 3.6) and shows that not too much is lost by the approximations involved in the stitching construction. Figure 10 compare the same stitched boundary to related bounds from the literature; our bound shows slightly improved constants over the best known bounds.

Although our stitching construction begins with a sub-gamma assumption, it applies to other sub- $\psi$ cases, including sub-Bernoulli, sub-Poisson and sub-exponential cases; see Figure 2 and Proposition 3. Further, our stitched bounds apply equally well in continuous-time settings to Brownian motion, continuous martingales, martingales with bounded jumps, and martingales whose jumps satisfy a Bernstein condition; see Corollary 35.

While our focus is on nonasymptotic results, Theorem 5 makes it easy to obtain the following general upper asymptotic LIL, proved in Appendix A.2:

########## {caption="Corollary 6"}

Suppose $(S_t)$ is sub- $\psi$ with variance process $(V_t)$ and $\psi(\lambda) \sim \lambda^2 / 2$ as $\lambda \downarrow 0$. Then

$ \begin{align} \limsup_{t \to \infty} \frac{S_t}{\sqrt{2 V_t \log \log V_t}} \leq 1 \quad \text{on } \left\lbrace \sup_t V_t = \infty \right\rbrace. \end{align} $

3.2 Conjugate mixture boundaries

For appropriate choice of mixing distribution $F$, the integral $\int \exp \left\lbrace \lambda S_t - \psi(\lambda) V_t \right\rbrace \mathop{}!\mathrm{d} F(\lambda)$ will be analytically tractable. Since, under Definition 1, this mixture process is upper bounded by a mixture supermartingale $\int L_t(\lambda) \mathop{}!\mathrm{d} F(\lambda)$, such mixtures yield closed-form or efficiently computable curved boundaries, which we call conjugate mixture boundaries. This approach is known as the method of mixtures, one of the most widely-studied techniques for constructing uniform bounds ([23, 21, 24, 22, 25, 26, 27, 30]). Unlike the stitched bound of Theorem 5, which involves a small amount of looseness in the analytical approximations, mixture boundaries involve no such approximations and, in the sub-Gaussian case, are unimprovable in the sense described in Section 3.6. We restate the following standard idea behind the method of mixtures using our definitions, with a proof in Appendix A.3. The proof details a technical condition on product measurability which we require of $L_t$.

########## {caption="Lemma 7"}

For any probability distribution $F$ on $[0, \lambda_{\max})$ and $\alpha \in (0, 1)$,

$ \begin{align} \mathcal{M}\alpha(v) := \sup\Bigg\lbrace s \in \mathbb{R}: \underbrace{\int \exp \left\lbrace \lambda s - \psi(\lambda) v \right\rbrace \mathop{}!\mathrm{d} F(\lambda)}{\eqqcolon m(s, v)} < \frac{l_0}{\alpha} \Bigg\rbrace \end{align}\tag{8} $

is a sub- $\psi$ uniform boundary with crossing probability $\alpha$, so long as the supermartingale $(L_t)$ of Definition 1 is product measurable when the underlying probability space is augmented with the independent random variable $\lambda$.

For each of our conjugate mixture bounds, we compute $m(s, v)$ in closed-form. The boundary $u(v)$ can then be computed by numerically solving the equation $m(s, v) = l_0 / \alpha$ in $s$, as we show in Appendix D. When an identical sub- $\psi$ condition applies to $(-S_t)$ as well as $(S_t)$, we may apply a uniform boundary to both tails and take a union bound, obtaining a two-sided confidence sequence. However, mixing over $\lambda \in \mathbb{R}$ rather than $\lambda \in \mathbb{R}_{\geq 0}$ yields a two-sided bound directly, so in some cases we present two-sided variants along with their one-sided counterparts. We give details for the following conjugate mixture boundaries in Appendix A.3:

- one-, two-sided normal mixture boundaries (sub-Gaussian case);

- one-, two-sided beta-binomial mixture boundaries (sub-Bernoulli case);

- one-sided gamma-Poisson mixture boundary (sub-Poisson case); and

- one-sided gamma-exponential mixture boundary (sub-exponential case).

The two-sided normal mixture boundary has a closed form expression:

$ \begin{align} u(v) \coloneqq \sqrt{ (v + \rho) \log\left(\frac{l_0^2 (v + \rho)}{\alpha^2 \rho} \right) }. \end{align}\tag{9} $

The one-sided normal mixture boundary has a similar, closed-form upper bound, making these especially convenient. It is clear from Equation 9 that the normal mixture boundary grows as $\mathcal{O}(\sqrt{v \log v})$ asymptotically, and this rate is shared by all of our conjugate mixture boundaries. Indeed, Proposition 8 below, proved in Appendix A.4, shows that such a rate holds for any mixture boundary as given by Equation 8 whenever the mixing distribution is continuous with positive density at and around the origin, a property which holds for all mixture distributions used in our conjugate mixture boundaries, subject to regularity conditions on $\psi$ which hold for the CGF of any nontrivial, mean-zero r.v. and specifically for the five $\psi$ functions in Section 2.

########## {caption="Proposition 8"}

Assume $(i)$ $\psi$ is nondecreasing, $\psi(0) = \psi'(0_+) = 0$, $\psi''(0_+) = c > 0$, and $\psi$ has three continuous derivatives on a neighborhood including the origin; and $(ii)$ $F$ has density $f$ (w.r.t. Lebesgue) which is continuous and positive on a neighborhood including the origin. Then

$ \begin{align} \mathcal{M}_\alpha(v) = \sqrt{ v \left[c\log\left(\frac{c l_0^2 v}{2\pi \alpha^2 f^2(0)} \right) + o(1) \right]} \quad \text{as } v \to \infty. \end{align}\tag{10} $

Note that $f$ need not place mass on all of $[0, \lambda_{\max})$, only near the origin, for the asymptotic rate to hold. Proposition 8 shows how the asymptotic behavior of any such mixture bound depends only on the behavior of $\psi$ and $f$ near the origin, a result reminiscent of the central limit theorem. Analogous, related results for the sub-Gaussian special case using $\psi(\lambda) = \lambda^2 / 2$ can be found in [26], Section 4 and [46], Theorem 2, in some cases under weaker assumptions on $F$.

In contrast to previous derivations of conjugate mixture boundaries in the literature, all of our conjugate mixture boundaries include a common tuning parameter $\rho > 0$ which controls the sample size for which the boundary is optimized. Such tuning is critical in practice, as we explain in Section 3.5, but has been ignored in much prior work. Additionally, with the exception of the sub-Gaussian case, most prior work on the method of mixtures has focused on parametric settings. We instead emphasize the applicability of these bounds to nonparametric settings. For example, when the observations are bounded, one may construct a confidence sequence making use of empirical-Bernstein estimates (Theorem 13) based on our gamma-exponential mixture (Proposition 24). See Appendix J for other conditions in which mixture bounds yield nonparametric uniform boundaries.

3.3 Numerical bounds using discrete mixtures

In applications, one may not need an explicit closed-form expression so long as the bound can be easily computed numerically. Our discrete mixture method is an efficient technique for numerical computation of curved boundaries for processes satisfying Definition 1. It permits arbitrary mixture densities, thus producing boundaries growing at the rate $\mathcal{O}(\sqrt{v \log \log v})$. Recall that the shape of the stitched bound was determined by the user-specified function $h$. For the discrete mixture bound, one instead specifies a probability density $f$ over finite support $(0, \overline{\lambda}]$ for some $\overline{\lambda} \in (0, \lambda_{\max})$. We first discretize $f$ using a series of support points $\lambda_k$, geometrically spaced according to successive powers of some $\eta > 1$, and an associated set of weights $w_k$:

$ \begin{align} \lambda_k \coloneqq \frac{\overline{\lambda}}{\eta^{k+1/2}} \quad \text{and} \quad w_k \coloneqq \frac{\overline{\lambda} (\eta - 1) f(\lambda_k\sqrt{\eta})}{\eta^{k+1}} \quad \text{for} \quad k = 0, 1, 2, \dots. \end{align}\tag{11} $

########## {caption="Theorem 9: Discrete mixture bound"}

Fix $\psi: [0, \lambda_{\max}) \to \mathbb{R}$, $\alpha\in(0, 1)$, $\overline{\lambda} \in (0, \lambda_{\max})$, and a probability density $f$ on $(0, \overline{\lambda}]$ that is nonincreasing and positive. For supports $\lambda_k$ and weights $w_k$ defined in Equation 11,

$ \textup{DM}\alpha(v) \coloneqq \sup\left\lbrace s \in \mathbb{R} : \sum{k=0}^\infty w_k \exp \left\lbrace \lambda_k s - \psi(\lambda_k) v \right\rbrace < \frac{l_0}{\alpha} \right\rbrace,\tag{12} $

is a sub- $\psi$ uniform boundary with crossing probability $\alpha$.

We suppress the dependence of $\textup{DM}_\alpha$ on $f$, $l_0$, $\overline{\lambda}$ and $\eta$ for notational simplicity. Though Theorem 9 is a straightforward consequence of the method of mixtures, our choice of discretization Equation 11 makes it effective, broadly applicable, and easy to implement. See Appendix A.5 for the proof of this result. Figure 9 includes an example bound, demonstrating a slight advantage over stitching. Appendix A.6 describes a connection between the stitching and discrete mixture methods, including a correspondence between the alpha-spending function $h$ and the mixture density $f$. Finally, we note that the method can be applied even when $f$ is not monotone; one must simply choose the discretization Equation 11 more carefully, using known properties of $f$.

3.4 Inverted stitching for arbitrary boundaries

In the method of mixtures, we choose a mixing distribution $F$ and the machinery yields a boundary $\mathcal{M}\alpha$. Likewise, in the stitching construction of Theorem 5, we choose an error decay function $h$ and obtain a boundary $\mathcal{S}\alpha$. Here, we invert the procedure: we choose a boundary function $g(v)$ and numerically compute an upper bound on its $S_t$-upcrossing probability using a stitching-like construction.

########## {caption="Theorem 10"}

For any nonnegative, strictly concave function $g:~ \mathbb{R} \to \mathbb{R}$ and $v_{\max} > 1$, the function

$ \begin{align} u(v) \coloneqq \begin{cases} g(1 \vee v), & v \leq v_{\max}, \ \infty, & \text{otherwise} \end{cases} \end{align}\tag{13} $

is a sub-Gaussian uniform boundary with crossing probability at most

$ \begin{align} l_0 \inf_{\eta > 1} \sum_{k=0}^{\lceil \log_\eta v_{\max} \rceil} \exp \left\lbrace -\frac{2(g(\eta^{k+1}) - g(\eta^k))(\eta g(\eta^k) - g(\eta^{k+1}))} {\eta^k(\eta - 1)^2} \right\rbrace. \end{align}\tag{14} $

The proof is in Appendix A.7. For simplicity we restrict to the sub-Gaussian case; examination of the proof will show that the method applies in other sub- $\psi$ cases as well, since we simply apply Lemma 4 to appropriately chosen lines, but more involved numerical calculations will be necessary, as the closed-form Equation 14 no longer applies. A similar idea was considered by [24], using a mixture integral approximation instead of an epoch-based construction to derive closed-form bounds. Theorem 10 requires numerical summation but yields tighter bounds with fewer assumptions. As an example, Theorem 10 with $\eta = 2.99$ shows that

$ \begin{align} \mathbb{P}\left(\exists t : 1 \leq V_t \leq 10^{20} \text{ and } S_t \geq 1.7 \sqrt{V_t (\log\log(e V_t) + 3.46)} \right) \leq 0.025. \end{align}\tag{15} $

This boundary is illustrated in Figure 9.

3.5 Tuning boundaries in practice

All uniform boundaries involve a tradeoff of tightness at different intrinsic times: making a bound tighter for some range of times requires making it looser at other times. Roughly speaking, the choice of a uniform boundary involves choosing both what time the bound should be optimized for (e.g., should the bound be tightest around 100 observations or around 100, 000 observations?) as well as how quickly the bound degrades as we move away from the optimized-for time (e.g., if we optimize for 100 samples, will the bound be twice as wide when we reach 1, 000 samples, or will it stay within a factor of two until we reach 1, 000, 000 samples?). A boundary which decays more slowly will necessarily not be as tight around the optimized-for time. In brief, linear boundaries decay the most quickly, conjugate mixture boundaries decay substantially more slowly, and polynomial stitched boundaries decay even more slowly; we feel that mixture boundaries strike a good balance in practice.

Here, we explain how to optimize uniform boundaries for a particular time and discuss the above tradeoff in more detail. Let $W_{-1}(x)$ be the lower branch of the Lambert $W$ function, the most negative real-valued solution in $z$ to $z e^z = x$. Consider the unitless process $S_t / \sqrt{V_t}$, and the corresponding uniform boundary $v \mapsto u(v) / \sqrt{v}$. Since all of our uniform boundaries $u(v)$ have positive intercept at $v = 0$, and all grow at least at the rate $\sqrt{v \log \log v}$ as $v \to \infty$, the normalized boundary $u(v) / \sqrt{v}$ diverges as $v \to 0$ and $v \to \infty$. For the two-sided normal mixture Equation 9, there is a unique time $m$ at which $u(v) / \sqrt{v}$ is minimized; $m$ is proportional to tuning parameter $\rho$ as follows:

![**Figure 4:** Comparison of normalized uniform boundaries $u(v) / \sqrt{v}$ optimized for different intrinsic times. Normal mixture uses Appendix Proposition 21, while gamma mixture uses Appendix Proposition 24. Polynomial stitched boundary is given in Equation 6, with $\eta = 2$ and $s = 1.4$. Discrete mixture applies Theorem 9 to the density $f(\lambda) = 0.4 \cdot 1_{0 \leq \lambda \leq 0.38} / [\lambda \log^{1.4}(0.38e / \lambda)]$ with $\eta = 1.1$, and $\lambda_{\max} = 0.38$; see Appendix A.6 for motivation. All boundaries use $\alpha = 0.025$.](https://ittowtnkqtyixxjxrhou.supabase.co/storage/v1/object/public/public-images/zn89zdcd/normalized_boundaries_paper.png)

########## {caption="Proposition 11"}

Let $u(v)$ be the two-sided normal mixture boundary Equation 9 with parameter $\rho > 0$.

- (a) For fixed $\rho > 0$, the function $v \mapsto u(v) / \sqrt{v}$ is uniquely minimized at $v = m$ with $m$ given by

$ \begin{align} \frac{m}{\rho} = -W_{-1}\left(-\frac{\alpha^2}{e l_0^2} \right) - 1. \end{align}\tag{16} $

- (b) For fixed $m > 0$, the choice of $\rho$ which minimizes the boundary value $u(m)$ is also determined by Equation 16.

The above result is proved in Appendix C.1; it is a matter of elementary calculus, but addresses a question that has received little attention in the literature. Figure 4 includes the normalized versions of two normal mixture boundaries optimized for different times, $m = 300$ and $m = $ 5, 000. Optimizing for the range of values of $V_t$ most relevant in a particular application will yield the tightest confidence sequences. However, as the figure shows, one need not have a very precise range of times, so long as one uses a conservatively low value for $m$, because $u(v) / \sqrt{v}$ grows slowly after time $m$. Indeed, for the normal mixture boundary with $\alpha = 0.05$ and $l_0 = 1$, we have $u(m) / \sqrt{m} \approx 3.0$ and $u(100m) / \sqrt{100m} \approx 3.6$, so that the penalty for being off by two orders of magnitude is modest.

The one-sided normal mixture boundary of Appendix Proposition 21 with crossing probability $\alpha$ is nearly identical to the two-sided normal mixture boundary with crossing probability $2\alpha$, so one may choose $\rho$ as in Proposition 11 with $\alpha$ doubled. For the gamma-exponential mixture and other non-sub-Gaussian uniform boundaries, Proposition 11 provides a good approximation in practice. Figure 4 includes gamma-exponential mixture boundaries with the same $\rho$ values as each corresponding normal mixture boundary. Though the normalized gamma-exponential mixture boundary with $m = 300$ clearly reaches its minimum at $v > m$, this choice of $\rho$ seems reasonable. Discrete mixtures can be similarly tuned by adjusting the precision of the mixing distribution, but require additional considerations (Appendix E).

Comparing the sub-Gaussian stitched boundary, discrete mixture boundary, and normal mixture boundary optimized for $m = 300$ in Figure 4 illustrates another important point for practice: although the normal mixture bound grows more quickly than the others as $v \to \infty$, it remains smaller over about three orders of magnitude. This makes it preferable for many real-world applications, as the longest feasible duration of an experiment is rarely more than two orders of magnitude larger than the earliest possible stopping time. For example, many online experiments run for at least one week to account for weekly seasonality effects, and very few such experiments last longer than 100 weeks. As both the normal mixture and the discrete mixture are unimprovable in general (Section 3.6), the difference is attributable to the choice of mixture, or alternatively, to the fact that the normal mixture trades tightness around the optimized-for time in exchange for looseness at much later times. The lesson is that the $\mathcal{O}(v \log \log v)$ rate, while asymptotically optimal in certain settings and useful for theory and some applications, may not be preferable in all real-world scenarios.

3.6 Unimprovability of uniform boundaries

Definition 2 of a sub- $\psi$ boundary $u$ involves only an upper bound on the $u$-crossing probability of any sub- $\psi$ process $(S_t)$. One may reasonably ask for corresponding lower bounds on the $u$-crossing probability to quantify how tight this boundary is. In the ideal case, we might desire a boundary $u$ such that the true $u$-crossing probability of some process $(S_t)$ is equal to the upper bound. In nonparametric settings, we cannot achieve this goal for every sub- $\psi$ process. However, we might still ask that there exists some sub- $\psi$ process for which the true $u$-crossing probability is arbitrarily close to the upper bound, so that the upper bound on crossing probability is unimprovable in general. That is, we might ask that the inequality on the supremum in Definition 2 holds with equality.

The fact we wish to point out, known in various forms, is that in the scalar, sub-Gaussian case, exact mixture bounds are unimprovable in the above sense. It is in this sense that the discrete mixture bound in Figure 9 provides a lower bound, showing that the sub-Gaussian polynomial stitched bound cannot be improved by much. The following result shows that, for any exact, sub-Gaussian mixture boundary $\mathcal{M}\alpha$, as defined in Lemma 7 for $\psi = \psi_N$, there exists a sub-Gaussian process whose true $\mathcal{M}\alpha$-crossing probability is arbitrarily close to $\alpha$. The result is similar to Theorem 2 of [26], which gives a more general invariance principle, but requires conditions on the boundary that appear difficult to verify for arbitrary mixture boundaries $\mathcal{M}\alpha$. Recall that $\mathbb{S}{\psi_N}^1$ is the class of pairs of processes $(S_t, V_t)$ such that $(S_t)$ is 1-sub-Gaussian with variance process $(V_t)$.

########## {caption="Proposition 12"}

For any exact, 1-sub-Gaussian mixture boundary $\mathcal{M}_\alpha$,

$ \begin{align} \sup_{(S_t, V_t) \in \mathbb{S}{\psi_N}^1} \mathbb{P}(\exists t \geq 1: S_t \geq \mathcal{M}\alpha(V_t)) = \alpha. \end{align} $

We prove Proposition 12 in Appendix C.2. In general, for each $\alpha$ there is an infinite variety of boundaries that are unimprovable in the above sense, differing in when they are loose and tight. These different boundaries will yield confidence sequences which are loose or tight at different sample sizes, or, equivalently, are efficient for detecting different effect sizes. Such a boundary cannot be tightened everywhere without increasing the crossing probability.

4. Applications

Section Summary: This section explores practical uses of a new statistical tool called an empirical-Bernstein confidence sequence, which helps estimate averages from bounded data by adapting to the observed variability rather than relying on worst-case assumptions. It begins by detailing the method's core theorem, which provides anytime-valid confidence intervals around the true average expectation, using predictions like past averages or more sophisticated forecasts to tighten the bounds without needing identical distributions. As an example, the approach is applied to measure average treatment effects in randomized experiments, employing an inverse probability weighting estimator to track causal impacts over time with guaranteed coverage.

After presenting an empirical-Bernstein confidence sequence for bounded observations, we apply our uniform boundaries to causal effect estimation and matrix martingales. We also consider estimation for a general, one-parameter exponential family.

4.1 An empirical-Bernstein confidence sequence

The following novel result is proved in Appendix A.8 using a self-normalization argument, which leads to its attractive simplicity. Recall the estimand $\mu_t \coloneqq t^{-1} \sum_{i=1}^t \mathbb{E}_{i-1} X_i$, the average conditional expectation.

########## {caption="Theorem 13"}

Suppose $X_t \in [a, b]$ a.s. for all $t$. Let $(\widehat{X}_t)$ be any $[a, b]$-valued predictable sequence, and let $u$ be any sub-exponential uniform boundary with crossing probability $\alpha$ for scale $c = b - a$. Then

$ \begin{align} \mathbb{P}\left(\forall t \geq 1: \left\lvert\bar{X}t - \mu_t\right\rvert < \frac{u\left(\sum{i=1}^t (X_i - \widehat{X}_i)^2 \right)}{t} \right) \geq 1 - 2\alpha. \end{align}\tag{17} $

This is an empirical-Bernstein bound because it uses the sum of observed squared deviations to estimate the true variance, much like a classical $t$-test. Hence the confidence radius scales with the true standard deviation for sufficiently large samples, regardless of the support diameter $b - a$, and with no prior knowledge of the true variance. Note also that this bound does not require that observations share a common mean.

The confidence statement Equation 17 holds for any sequence of predictions $(\widehat{X}_i)$, but predictions closer to the conditional expectations, $\widehat{X}i \approx \mathbb{E}{i-1} X_i$, will yield smaller confidence intervals on average. A simple choice is the mean, $\widehat{X}t = (t-1)^{-1} \sum{i=1}^{t-1} X_i$, which will be effective when the samples are i.i.d., for example. But the predictions $(\widehat{X}_i)$ can also make use of trends, seasonality, stratification or regression (in the presence of covariates), machine learning algorithms, or any other information that may aid with prediction.

For an explicit example, assume $X_i \in [0, 1]$ and define the empirical variance as $\widehat{V}t \coloneqq \sum{i=1}^t (X_i - \bar{X}_{i-1})^2$. Invoking Theorem 13 with the polynomial stitched bound Equation 6 using $c=1$, $\eta=2$, $m=1$, and $h(k) \propto k^{1.4}$, we have the following 95%-confidence sequence for $\mu_t$:

$ \begin{align} \smash{ \bar{X}_t \pm \frac{ 1.7 \sqrt{(\widehat{V}_t \vee 1) (\log \log(2(\widehat{V}_t \vee 1)) + 3.8)}

- 3.4 \log \log(2(\widehat{V}_t \vee 1)) + 13 }{t}.} \end{align}\tag{18} $

When a closed form is not required, the gamma-exponential mixture (Proposition 24) may yield tighter bounds than stitching; simulations in Section 5 demonstrate the use of Theorem 13 with this mixture.

4.2 Estimating ATE in the Neyman-Rubin model

As one illustration of Theorem 13, we consider the sequential estimation of average treatment effect under the Neyman-Rubin potential outcomes model ([47, 48, 49]). We imagine a sequence of experimental units, each with real-valued potential outcomes under control and treatment denoted by ${Y_t(0), Y_t(1)}_{t \in \mathbb{N}}$, respectively. These potential outcomes are fixed, but we observe only one outcome for each unit in the experiment. We assign a randomized treatment to each unit, denoted by the $\lbrace 0, 1 \rbrace$-valued random variable $Z_t \in \mathcal{F}t$, observing $Y_t^\textup{obs} \coloneqq Y_t(Z_t)$. Here treatment is assigned by flipping a coin for each subject, with a bias possibly depending on previous observations. This treatment assignment is the only source of randomness. Specifically, let $P_t \coloneqq E{t-1} Z_t$ and suppose $0 < P_t < 1$ a.s. for all $t$; then we permit $P_t$ to vary between individuals and to depend on past outcomes. This accommodates Efron's biased coin design [50] and related covariate balancing methods.

At each step $t$, having treated and observed units $1, \dots, t$, we wish to draw inference about the estimand $\textup{ATE}t \coloneqq t^{-1} \sum{i=1}^t [Y_i(1) - Y_i(0)]$. In particular, we seek a confidence sequence for $(\textup{ATE}t){t=1}^\infty$. To construct our estimator, we may utilize any predictions $\widehat{Y}_t(0)$ and $\widehat{Y}t(1)$ for each unit's potential outcomes; these random variables must be $\mathcal{F}{t-1}$-measurable, for each $t$. We then employ the inverse probability weighting estimator

$ \begin{align} X_t & \coloneqq \widehat{Y}_t(1) - \widehat{Y}_t(0)

- \left(\frac{Z_t - P_t}{P_t(1 - P_t)} \right) (Y_t^\textup{obs} - \widehat{Y}_t(Z_t)), \end{align}\tag{19} $

which is (conditionally) unbiased for the individual treatment effect $Y_t(1) - Y_t(0)$. As with Theorem 13, better predictions will lead to shorter confidence intervals, but the coverage guarantee holds for any choice of predictions, and a reasonable choice would be the average of past observed outcomes. See [51] for a similar strategy for fixed-sample estimation.

We assume bounded potential outcomes; for simplicity we assume $Y_t(k) \in [0, 1]$ for all $t \geq 1, k = 0, 1$, and we assume predictions are likewise bounded. We further assume that treatment probabilities are uniformly bounded away from zero and one. Then, an empirical-Bernstein confidence sequence for $\textup{ATE}_t$ follows from Theorem 13, where we use $\widehat{X}_t = \widehat{Y}_t(1) - \widehat{Y}_t(0)$ so that

$

\begin{align}

V_t ~ \coloneqq~ \sum_{i=1}^t (X_i - \widehat{X}i)^2

= \sum{i=1}^t \left(\frac{Z_i - P_i}{P_i(1 - P_i)} \right)^2 (Y_i^\textup{obs} - \widehat{Y}_i(Z_i))^2.

\end{align}

$

########## {caption="Corollary 14"}

Suppose $P_t \in [p_{\min}, 1 - p_{\min}]$ a.s., $Y_t(k) \in [0, 1]$ and $\widehat{Y}t(k) \in [0, 1]$ for all $t \geq 1, k = 0, 1$. Let $u$ be any sub-exponential uniform boundary with scale $2 / p{\min}$ and crossing probability $\alpha$. Then

$ \begin{align} \mathbb{P}\left(\forall t \geq 1: \left\lvert\bar{X}_t - \textup{ATE}_t\right\rvert < \frac{u(V_t)}{t} \right) \geq 1 - 2\alpha. \end{align} $

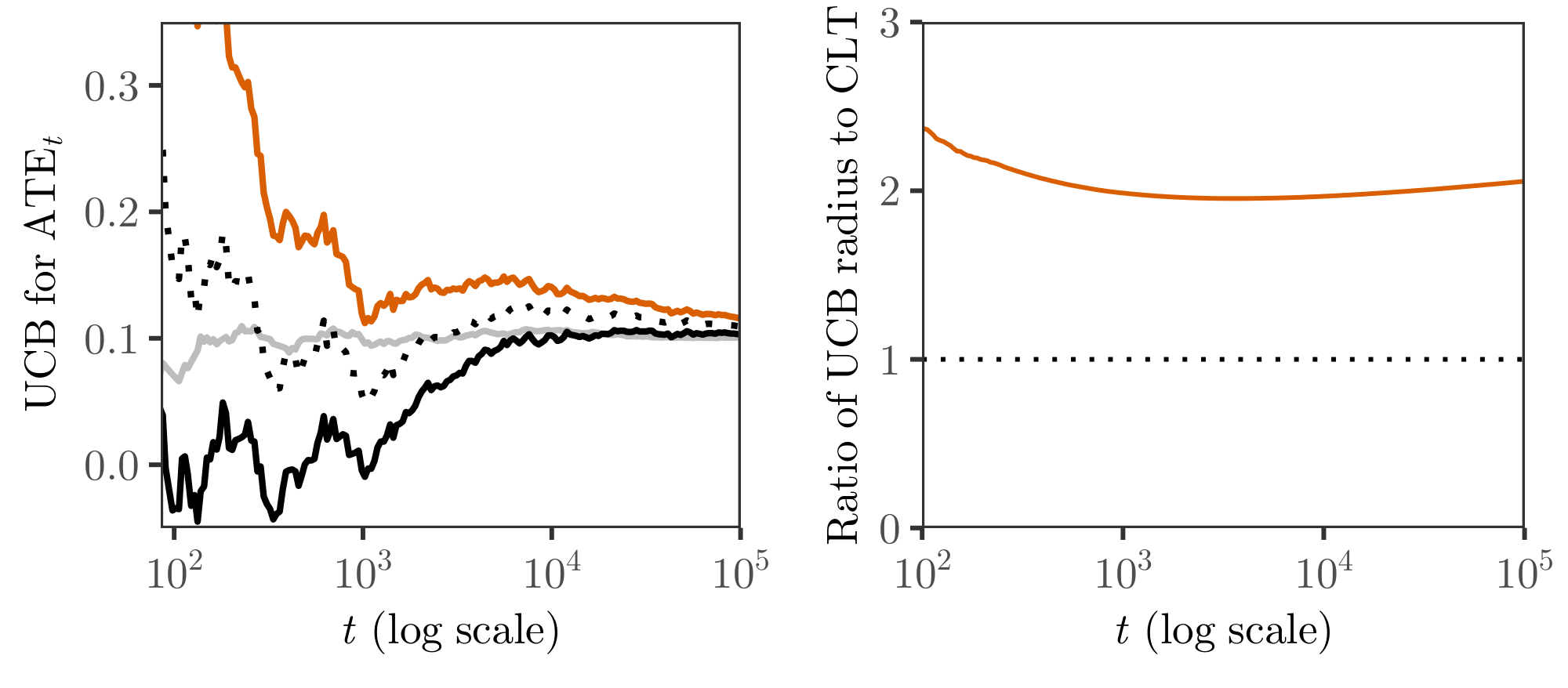

For $u$, one may choose the gamma-exponential mixture boundary (Proposition 24) or the stitched boundary Equation 6 with $c=\frac{2}{p_{\min}}$. Figure 5 illustrates our strategy on simulated data. Over the range $t = 100$ to $t = $ 100, 000 displayed, our bound is about twice as wide as the fixed-sample CLT bound, with the ratio growing at a slow $ \mathcal{O}(\sqrt{\log t})$ rate thereafter. Of course the fixed-sample CLT bound provides no uniform coverage guarantee.

4.3 Matrix iterated logarithm bounds

Our second application is the construction of iterated logarithm bounds for random matrix sums and their use in sequential covariance matrix estimation. The curved uniform bounds given in Section 3 may be applied to matrix martingales by taking $(S_t)$ to be the maximum eigenvalue process of the martingale and $(V_t)$ the maximum eigenvalue of the corresponding matrix variance process. [6], Section 2 give sufficient conditions for Definition 1 to hold in this matrix case. Then Theorem 5 yields a novel matrix finite LIL; here we give an example for bounded increments. We denote the space of symmetric, real-valued, $d \times d$ matrices by $\mathbb{S}^d$; $\gamma_{\max}(\cdot)$ denotes the maximum eigenvalue; $\ell_{\eta, s}(v) = s \log\log(\eta v / m) + \log \frac{d, \zeta(s)}{\alpha \log^s \eta}$; and $k_1(\eta), k_2(\eta)$ are defined in Equation 4.

########## {caption="Corollary 15"}

Suppose $(Y_t){t=1}^\infty$ is a $\mathbb{S}^d$-valued matrix martingale such that $\smash{\gamma{\max}(Y_t - Y_{t-1}) \leq b}$ a.s. for all $t$. Let $V_t \coloneqq \gamma_{\max}(\sum_{i=1}^t \mathbb{E}{t-1} (Y_t - Y{t-1})^2)$ and $S_t \coloneqq \gamma_{\max}(Y_t)$. Then for any $\smash{\eta >1, s>1, m>0, \alpha\in(0, 1)}$, we have

$ \mathbb{P}\left(\exists t \geq 1 : S_t \geq k_1(\eta) \sqrt{(V_t \vee m) \ell_{\eta, s}(V_t \vee m)}

- \frac{b k_2(\eta)}{3} \ell_{\eta, s}(V_t \vee m) \right) \leq \alpha.\tag{20} $

The result follows using the polynomial stitched boundary after invoking Fact 1(c) and Lemma 2 of [6] (cf. ([52])), which show that $(S_t)$ is sub-gamma with variance process $(V_t)$, scale $c = b/3$, and $l_0 = d$. Beyond bounded increments, the same bound holds for any sub-gamma process. As evidenced by Proposition 3, this is a very general condition.

Taking $\eta$ and $s$ arbitrarily close to one and using the final result of Theorem 5, we obtain the following asymptotic matrix upper LIL, proved in Appendix A.9. Here we denote the martingale increments by $\Delta Y_t \coloneqq Y_t - Y_{t-1}$.

########## {caption="Corollary 16"}

Let $(Y_t){t=1}^\infty$ be a $\mathbb{S}^d$-valued, square-integrable martingale, and define $V_t = \gamma{\max}\left(\sum_{i=1}^t \mathbb{E}_{i-1} \Delta Y_t^2 \right)$. Then

$ \begin{align} \limsup_{t \to \infty} \frac{\gamma_{\max}\left(Y_t \right)} {\sqrt{2 V_t \log \log V_t}} \leq 1 \quad \text{a.s. on } \left\lbrace \sup_t V_t = \infty \right\rbrace \end{align}\tag{21} $

whenever either (1) the increments $(\Delta Y_t)$ are i.i.d., or (2) the increments $(\Delta Y_t)$ satisfy a Bernstein condition on higher moments: for some $c > 0$, for all $t$ and all $k > 2$, $\mathbb{E}{t-1} (\Delta Y_t)^k \preceq (k!/2) c^{k-2} \mathbb{E}{t-1} \Delta Y_t^2$.

The Bernstein condition holds if the increments are uniformly bounded, $\gamma_{\max}(\Delta Y_t) \leq c$ for some $c > 0$. Also, in the i.i.d. case, $\mathbb{P}(V_t \to \infty) = 1$ and then Equation 21 states that $\smash{\limsup_{t \to \infty} \gamma_{\max}\left(Y_t \right) / \sqrt{2 \gamma_{\max}(\mathbb{E} \Delta Y_1^2) t \log \log t} \leq 1}$, a.s. on $\lbrace \sup_t V_t = \infty \rbrace$. When $d = 1$, this recovers the classical upper LIL, showing that Corollary 16 cannot be improved uniformly, but we are not aware of an appropriate lower bound for the general matrix case.

We now consider the nonasymptotic sequential estimation of a covariance matrix based on bounded vector observations ([53, 54, 55, 56, 57]). In particular, we observe a sequence of independent, mean zero, $\mathbb{R}^d$-valued random vectors $x_t$ with common covariance matrix $\Sigma = \mathbb{E} x_t x_t^T$. We wish to estimate $\Sigma$ using an operator-norm confidence ball centered at the empirical covariance matrix $\widehat{\Sigma}t \coloneqq t^{-1} \sum{i=1}^t x_i x_i^T$. For fixed-sample estimation, when $\lVert x_i\rVert_2 \leq \sqrt{b}$ a.s. for all $i \in [t]$, the analysis of [56], section 1.6.3 implies

$ \begin{align} {\mathbb{P}\left(\lVert\widehat{\Sigma}t - \Sigma\rVert{\text{op}} \geq \sqrt{\frac{2 b \lVert\Sigma\rVert_{\text{op}} \log(2d/\alpha)}{t}}

- \frac{4 b \log(2d/\alpha)}{3t} \right) \leq \alpha.} \end{align}\tag{22} $

We use a sub-Poisson uniform boundary to obtain a uniform analogue:

########## {caption="Corollary 17"}

Let $(x_t)_{t=1}^\infty$ be a sequence of $\mathbb{R}^d$-valued, independent random vectors with $\mathbb{E} x_t = 0$, $\lVert x_t\rVert_2 \leq \sqrt{b}$ a.s. and $\mathbb{E} x_t x_t^T = \Sigma$ for all $t$. If $u$ is a sub-Poisson uniform boundary with crossing probability $\alpha$ and scale $2b$, then

$ \begin{align} \mathbb{P}\left(\exists t \geq 1 : \lVert\widehat{\Sigma}t - \Sigma\rVert{\text{op}} \geq \frac{1}{t} u\left(b t \lVert\Sigma\rVert_{\text{op}} \right) \right) \leq \alpha. \end{align} $

For example, using the polynomial stitched bound with scale $c = 2b/3$ and $m = b \lVert\Sigma\rVert_{\text{op}}$, Corollary 17 gives a $(1-\alpha)$-confidence sequence for $\Sigma$ with operator norm radius $\mathcal{O}(\sqrt{t^{-1} \log \log t})$. This bound has the closed form

$ {\mathbb{P}\left(\exists t \geq 1 : \lVert\widehat{\Sigma}t - \Sigma\rVert{\text{op}} \geq k_1 \sqrt{\frac{b \lVert\Sigma\rVert_{\text{op}} \ell(t)}{t}}

- \frac{4b k_2 \ell(t)}{3t} \right) \leq \alpha, }\tag{23} $

where $\ell(t) = s \log\log(\eta t) + \log \frac{d, \zeta(s)}{\alpha \log^s \eta}$, and $k_1, k_2$ are defined in Equation 4.

In other words, with high probability, we have for all $t \geq 1$ that

$ \begin{align} {\lVert\widehat{\Sigma}t - \Sigma\rVert{\text{op}} \lesssim \sqrt{\frac{b \log(d\log t)}{t}} + \frac{b \log(d\log t)}{t}.} \end{align} $

Compared to the fixed-sample result Equation 22, we obtain uniform control by adding a factor of $\log \log t$. We are not aware of other results like these for sequential covariance matrix estimation. Figure 6 illustrates the confidence sequence of Corollary 17 on simulated data using a discrete mixture boundary with the mixture density $f^{\text{LIL}}_s$ defined in Equation 41.

4.4 One-parameter exponential families

Suppose $(X_t)$ are i.i.d. from an exponential family in mean parametrization, with sufficient statistic $T(X)$ having mean in some set $\Omega$. For each $\mu \in \Omega$, we write the density as $\smash{f_{\mu}(x) = h(x) \exp \left\lbrace \theta(\mu) T(x) - A(\theta(\mu)) \right\rbrace}$ where $A'(\theta(\mu)) = \mu$. Let $\psi_\mu$ be the cumulant-generating function of $T(X_1) - \mu$ when $\mathbb{E} T(X_1) = \mu$, that is, $\smash{\psi_\mu(\lambda) \coloneqq A(\lambda + \theta(\mu)) - A(\theta(\mu)) - \lambda \mu}$, with $\psi_\mu(\lambda) \coloneqq \infty$ if the RHS does not exist. Writing $S_t(\mu) \coloneqq \sum_{i=1}^t T(X_i) - t \mu$, the process $\exp \left\lbrace \lambda S_t(\mu) - t \psi_\mu(\lambda) \right\rbrace$ is the likelihood ratio testing $H_0: \theta = \theta(\mu)$ against $H_1: \theta = \theta(\mu) + \lambda$, and if we use a method-of-mixtures uniform boundary, the resulting confidence sequence will be dual to a family of mixture sequential probability ratio tests, as discussed in Section 6. To obtain a two-sided confidence sequence, we use the "reversed" CGF $\tilde{\psi}\mu(\lambda) = \psi\mu(-\lambda)$. We summarize these observations as follows; see [27], Theorem 1 for a related result.

########## {caption="Corollary 18"}

Suppose, for each $\mu \in \Omega$, $u_\mu$ is a sub- $\psi_\mu$ uniform bound with crossing probability $\alpha_1$, and $\tilde{u}\mu$ is a sub- $\tilde{\psi}\mu$ uniform bound with crossing probability $\alpha_2$. Defining

$ \begin{align} \textup{CI}t \coloneqq \left\lbrace \mu \in \Omega: -\tilde{u}\mu(t) < S_t(\mu) < u_\mu(t) \right\rbrace, \end{align}\tag{24} $

we have $\mathbb{P}(\forall t \geq 1: \mathbb{E} T(X_1) \in \textup{CI}_t) \geq 1 - \alpha_1 - \alpha_2$.

5. Simulations

Section Summary: This section presents simulations testing various confidence sequence methods for estimating the average of sequences of bounded random numbers, using 1,000 runs each with 100,000 observations from three different distributions. In the simplest case, a balanced coin-flip-like distribution, most methods effectively control errors and produce reasonably narrow intervals, but in a skewed case with rare events, basic bounds become overly wide while smarter approaches that infer variance from the data perform better and keep errors in check. For the most challenging three-point distribution with occasional extreme values, only the method using an adaptive variance estimate from past data delivers tight, reliable intervals without failing to cover the true average.

In[^1] Figure 7 we illustrate the error control of some of our confidence sequences for estimating the mean of an i.i.d. sequence of observations $(X_i)$ with bounded support $[a, b]$. We compare four strategies:

[^1]: The repository https://github.com/gostevehoward/cspaper contains code to reproduce all simulations and plots in this paper. Uniform boundaries themselves are implemented in R and Python packages at https://github.com/gostevehoward/confseq.

- The Hoeffding strategy exploits the fact that bounded observations are sub-Gaussian ([37]; cf. [6], Lemma 3(c)). We use a two-sided normal mixture boundary Equation 9 with variance process $V_t = (b-a)^2 t / 4$.

- The beta-binomial strategy uses the stronger condition that bounded observations are sub-Bernoulli ([37]; cf. [6], Fact 1(b)), accounting for the true mean as well as the boundedness, but possibly failing to take account of the true variance. For hypothesized true mean $\mu$, this strategy uses the beta-binomial mixture boundary given in Proposition 22, with parameters $g(\mu) = \mu - a$ and $h(\mu) = b - \mu$, and variance process $V_t(\mu) = g(\mu) h(\mu) t$. The confidence set for the mean is $\lbrace \mu \in [a, b]: -f_{g(\mu), h(\mu)}(V_t(\mu)) \leq \sum_{i=1}^t X_i - t \mu \leq f_{h(\mu), g(\mu)}(V_t(mu)) \rbrace$. This is more efficiently computed using the mixture supermartingale $m(S_t, V_t)$ of Equation 35, as $\lbrace \mu \in [a, b]: m(\sum_{i=1}^t X_i - t \mu, V_t(\mu)) < 1 / \alpha \rbrace$.

- The pointwise Bernoulli strategy uses the same sub-Bernoulli condition as the beta-binomial strategy, but relies on a fixed-sample Cramér-Chernoff bound which is valid pointwise but not uniformly over time. Specifically, we reject mean $\mu$ if $V_t \psi_B^\star(S_t / V_t) \geq \log \alpha^{-1}$, where $S_t$ is the sum of centered observations as usual, $V_t = (\mu - a)(b - \mu) t$, and we set $\smash{g = \mu - a, h = b - \mu}$ in $\psi_B$, with $\psi_B^\star$ its Legendre-Fenchel transform.

- The empirical-Bernstein strategy uses an empirical estimate of variance, thus achieving a confidence width scaling with the true variance in all three cases. Here we use Theorem 13 with a gamma-exponential mixture boundary (Proposition 24). For predictions, we use the mean of past observations: $\widehat{X}t = (t-1)^{-1} \sum{i=1}^{t-1} X_i$.